Cross-Validation in Machine Learning

Cross-validation is the single most important technique for honestly estimating how well your machine learning model will perform on data it has never seen. It works by systematically partitioning your dataset into complementary subsets -- training on some partitions and validating on the remaining ones -- and repeating this process multiple times to average out the noise in any single split.

Why does this matter so much? Because a model's performance on training data tells you almost nothing about its real-world performance. Every experienced ML practitioner has a horror story about a model that looked stellar on the training set and fell flat in production. Cross-validation is the antidote to this false confidence -- it provides a realistic, low-variance estimate of generalization error before you deploy anything.

From a data scientist at Flipkart evaluating product recommendation models across millions of SKUs, to a research team at IIT building medical diagnostic classifiers on small clinical datasets, cross-validation is the universal tool for model assessment. It is simultaneously simple enough to explain in five minutes and deep enough that getting it wrong leads to seriously misleading results.

This guide covers everything from basic K-fold to advanced techniques like nested CV, time-series CV, and GroupKFold, along with the data leakage pitfalls that even experienced practitioners stumble over, practical code examples using scikit-learn, and cost analysis relevant to Indian ML teams.

Concept Snapshot

- What It Is

- A resampling technique that partitions data into multiple train/validation splits to estimate a model's generalization performance, providing a more robust and less noisy estimate than a single holdout split.

- Category

- Model Training

- Complexity

- Intermediate

- Inputs / Outputs

- Inputs: a dataset and a model (or pipeline). Outputs: an array of performance scores (one per fold), their mean and standard deviation, and optionally per-fold predictions for every data point.

- System Placement

- Sits after train-test split (using only the training portion) and before or alongside hyperparameter tuning. In the simplest case, it replaces the single validation set with a rotation of validation sets.

- Also Known As

- CV, K-fold validation, cross-validation resampling, rotation estimation, out-of-fold evaluation

- Typical Users

- Data Scientists, ML Engineers, Research Scientists, Biostatisticians, Applied Scientists

- Prerequisites

- Train/test/validation splits, Overfitting and underfitting concepts, Basic statistics (mean, variance, confidence intervals), Model evaluation metrics (accuracy, F1, RMSE, etc.)

- Key Terms

- foldK-foldstratificationleave-one-outout-of-fold predictionsnested CVdata leakageGroupKFoldTimeSeriesSplitbias-variance tradeoffcross_val_score

Why This Concept Exists

The Problem With a Single Holdout Split

Imagine you have 10,000 labeled samples and you split them 80/20 into train and validation sets. You train a model, evaluate on the validation set, and get 92% accuracy. Is that a good estimate of how the model will perform in production?

The honest answer is: you have no idea. That particular 20% holdout might have been slightly easier or harder than the rest of the data. It might have missed certain edge cases, or overrepresented certain subgroups. If you had split differently, you might have gotten 89% or 95%. The variance of a single split is surprisingly high, especially for small to medium datasets.

This is the fundamental problem that cross-validation solves. By evaluating on every possible (or a representative sample of) validation splits and averaging the results, CV produces an estimate with dramatically lower variance.

A Brief History: From Stone to scikit-learn

The idea of cross-validation dates back to the 1930s (Larson, 1931), but the formal framework was established by Mervyn Stone in his landmark 1974 paper in the Journal of the Royal Statistical Society. Stone showed that leave-one-out cross-validation is asymptotically equivalent to Akaike's Information Criterion (AIC) for model selection -- a result that connected CV to the broader theory of statistical model selection.

Throughout the 1980s and 1990s, cross-validation became the standard evaluation methodology in statistics and machine learning. Dietterich (1998) published an influential paper analyzing the statistical properties of different CV-based comparison tests, showing that some commonly used approaches (like a paired t-test on 10-fold CV results) have elevated Type I error rates. This work shaped best practices for decades.

The modern era brought two critical developments: Varma and Simon (2006) formalized nested cross-validation for unbiased model selection, and Bergmeir, Hyndman, and Koo (2018) provided theoretical justification for applying standard CV to autoregressive time series models. Today, scikit-learn's cross_val_score, cross_validate, and the family of splitter classes (KFold, StratifiedKFold, GroupKFold, TimeSeriesSplit) have made cross-validation accessible to every Python practitioner.

Why It Remains Essential in the Deep Learning Era

You might ask: if I'm training a large neural network on millions of samples, do I still need cross-validation? For very large datasets, a single well-constructed holdout set is often sufficient because the variance of the performance estimate is already low. But cross-validation remains essential in several scenarios that are extremely common in practice:

- Small to medium datasets (under ~50K samples) -- medical imaging, NLP for low-resource Indian languages, fraud detection with rare events

- Model comparison -- when the difference between two models is small (0.5-2%), CV is the only way to tell if the difference is real or noise

- Hyperparameter tuning -- CV provides the evaluation signal that guides the search (it sits inside the tuning loop)

- Regulatory and compliance settings -- clinical trials, financial models, and insurance pricing require statistically rigorous evaluation that a single split cannot provide

Key Insight: Cross-validation is not just an evaluation technique -- it is a philosophy of honest model assessment. The moment you report a single holdout number as your model's performance, you are implicitly assuming that one random split is representative. CV makes you question that assumption.

Core Intuition & Mental Model

The Mental Model: Exam Preparation

Think of cross-validation like a student preparing for a final exam by taking practice tests. If the student takes just one practice test, their score on that specific test might be misleadingly high (they got lucky with the topics) or misleadingly low (the practice test overemphasized a weak area). The student has no way to separate their true ability from the noise of that one test.

But if the student takes five different practice tests, each covering different subsets of the material, and averages the scores, they get a much more reliable estimate of how they'll do on the real exam. Each practice test reveals different strengths and weaknesses, and the average smooths out the noise.

That is exactly what K-fold cross-validation does. Your dataset is the full study material, each fold is a different practice test, and the averaged score is your best estimate of true model performance.

The Key Twist: Every Data Point Gets Tested

What makes cross-validation elegant is that, across all folds, every single data point serves as a validation point exactly once. In 5-fold CV, each of the 5 folds gets its turn as the validation set while the other 4 form the training set. The final score is the average of 5 evaluation scores. This means you use 100% of your data for both training and evaluation (just not at the same time), which is especially valuable when data is scarce.

What Cross-Validation Is NOT

Let me be precise about the boundaries. Cross-validation is not a training technique -- it does not produce a better model. It is an evaluation technique that tells you how good a model (or modeling approach) is. The actual model you deploy is typically trained on the full training dataset after CV has helped you select the best approach.

Cross-validation also does not replace a held-out test set. The test set is your final, untouched evaluation after all model selection and tuning decisions have been made. CV operates on the training data to guide those decisions; the test set validates the final outcome.

Expert Note: The most common mistake I see in production ML is treating the CV score as the deployment performance estimate. CV tells you how good your procedure is (model + preprocessing + feature engineering), but the actual deployed model is trained on all the data and has no direct CV score. The test set performance is your deployment estimate.

Technical Foundations

Standard K-Fold Cross-Validation

Given a dataset and a learning algorithm , K-fold cross-validation partitions into approximately equal-sized disjoint subsets (folds) such that:

For each fold :

- Train the model on (all folds except fold )

- Evaluate on to get score

The cross-validation estimate is:

with standard error:

Bias-Variance Decomposition

The choice of involves a bias-variance tradeoff:

-

Small (e.g., ): Each training set has only samples, so models are trained on less data than the full training set. This introduces pessimistic bias -- the CV estimate is lower than the true performance of the model trained on all data.

-

Large (approaching , i.e., LOO): Each training set has samples, so bias is minimal. But the training sets are nearly identical, meaning the per-fold scores are highly correlated. This inflates variance -- the estimate becomes unstable.

-

or are the standard choices. Empirical studies (Kohavi, 1995; Hastie et al., 2009) show these values offer a good bias-variance tradeoff for most practical problems.

Leave-One-Out Cross-Validation (LOOCV)

The special case :

LOOCV has nearly zero bias (each model trains on samples) but can have high variance and is computationally expensive -- requiring model fits. However, for linear models, there is a closed-form shortcut using the hat matrix :

where is the -th diagonal element of and is the prediction from the full model. This computes LOOCV in the cost of a single model fit.

Stratified K-Fold

For classification, stratified K-fold ensures that each fold preserves the class distribution of the original dataset. If class has proportion in , then each fold also has approximately proportion of class . This is critical for imbalanced datasets where random splitting might produce folds with zero samples from the minority class.

Repeated K-Fold

Repeat the K-fold procedure times with different random shuffles, producing scores. The final estimate averages all scores, reducing variance at the cost of model fits.

Nested Cross-Validation

When cross-validation is used for both model selection and performance estimation, a nested (double) CV is required to avoid optimistic bias:

- Outer loop: folds for performance estimation

- Inner loop: folds (within each outer training set) for hyperparameter tuning / model selection

For each outer fold :

- Use the inner CV on to select the best hyperparameters

- Train the model with on the full

- Evaluate on

This ensures the performance estimate is unbiased because the outer test fold is never used in any model selection decision. The total number of model fits is where is the number of hyperparameter configurations tested.

Internal Architecture

A cross-validation system has four logical layers: a splitter that generates train/validation indices for each fold, a pipeline executor that runs the full preprocessing + training + evaluation pipeline for each fold, a metric aggregator that collects and summarizes per-fold results, and optionally an outer loop controller for nested CV that wraps the inner CV within a model selection step.

The architecture must enforce a strict information barrier: the validation fold of each iteration must be completely isolated from all preprocessing and training decisions. This is where data leakage occurs when the architecture is implemented incorrectly.

For nested CV, the inner loop replaces each fold's training step with a complete hyperparameter search, adding another level of splitting within the training partition of each outer fold.

Key Components

Fold Splitter

Generates the index arrays for each fold. Implements the splitting strategy: KFold for basic splitting, StratifiedKFold for preserving class distributions, GroupKFold for respecting group boundaries (e.g., patients, users), or TimeSeriesSplit for temporal data. The splitter is the single source of truth for which samples belong to training vs. validation in each iteration.

Pipeline Executor

Runs the complete modeling pipeline for each fold: preprocessing (scaling, encoding, imputation), feature engineering, model training, and evaluation. Critical: all preprocessing must be fit on the training fold only and then applied (transformed) to the validation fold. This is where sklearn.pipeline.Pipeline is essential -- it ensures preprocessing and training are coupled correctly within each fold.

Metric Aggregator

Collects per-fold scores, computes the mean, standard deviation, and confidence intervals. May also aggregate per-fold predictions (out-of-fold predictions) to produce a full-dataset prediction for downstream analysis like stacking or calibration.

Out-of-Fold Prediction Collector

For each fold, saves the model's predictions on the validation portion. After all folds complete, these predictions are stitched together to form a complete prediction for every sample in the dataset, with each prediction made by a model that never saw that sample during training. Used for model stacking and calibration curve analysis.

Nested CV Outer Loop Controller

In nested cross-validation, this component manages the outer fold loop and delegates model selection (hyperparameter tuning) to the inner loop. It ensures that the inner loop's search space and selection criterion are applied independently within each outer fold, preventing information leakage from the outer evaluation into the model selection process.

Data Flow

Split Phase: The fold splitter generates sets of (train_indices, val_indices) pairs. For stratified splitting, class labels are used to ensure proportional representation. For group splitting, group identifiers ensure no group spans both train and validation.

Execute Phase: For each fold, the pipeline executor receives the training indices and validation indices. It subsets the data, fits all preprocessing steps on the training data, transforms both training and validation data, trains the model, and generates predictions on the validation data. The evaluation metric is computed and stored.

Aggregate Phase: After all folds complete, the metric aggregator computes summary statistics. The out-of-fold prediction collector concatenates validation predictions in the correct order to reconstruct a full-dataset prediction.

Nested Phase (if applicable): Each fold's training data is itself split into inner folds for hyperparameter search. The best hyperparameters from the inner loop are used to train the final model for that outer fold.

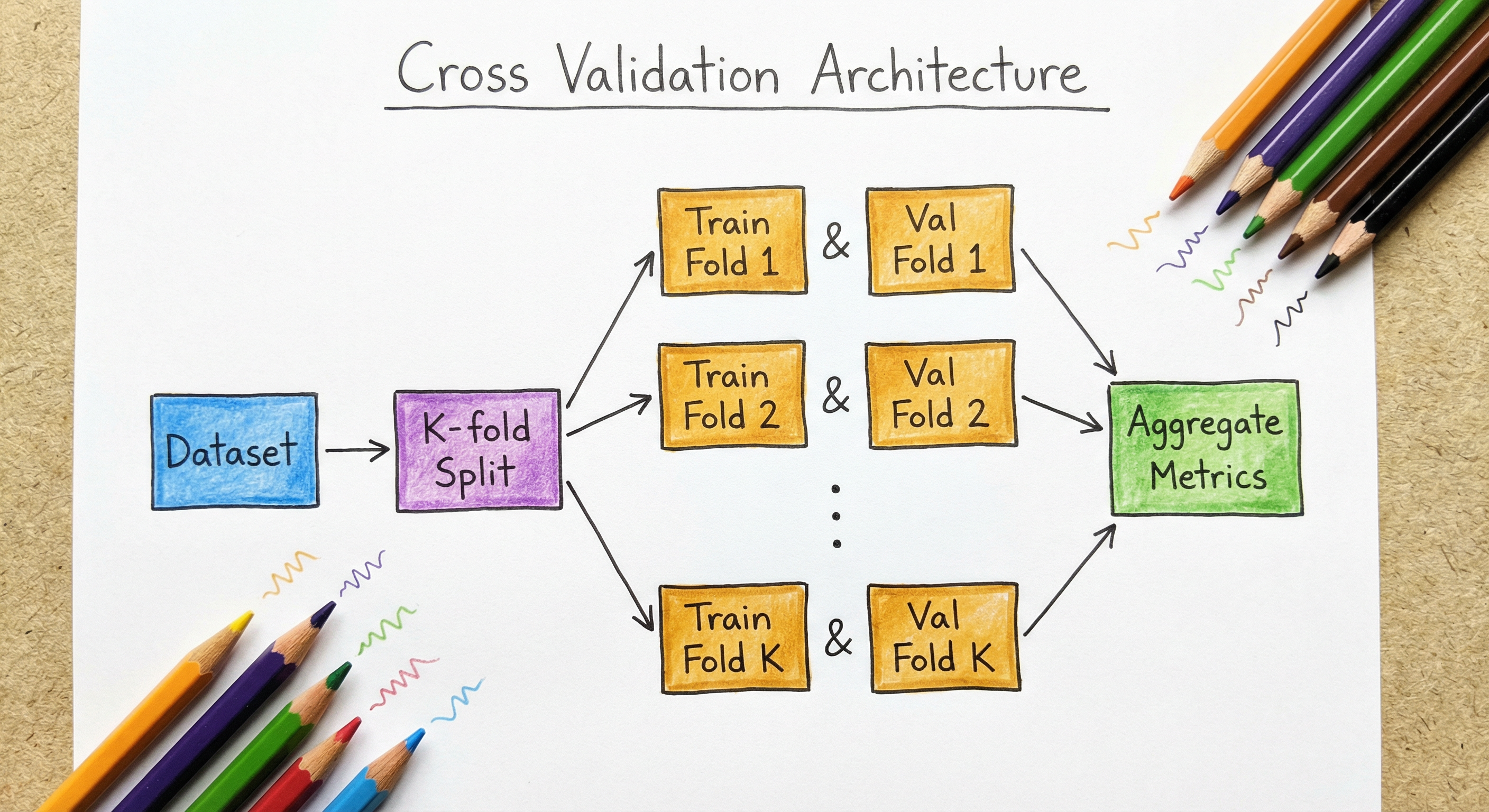

A vertical flow from 'Full Training Dataset' to 'Splitter (KFold / StratifiedKFold / GroupKFold / TimeSeriesSplit)', which fans out to 5 parallel fold executions (Fold 1 through Fold 5, each showing its train/validate partition). All 5 folds feed into a 'Metric Aggregator' which produces the final 'Mean Score +/- Std Dev + Per-Fold Breakdown'.

How to Implement

Implementation Approaches

Cross-validation implementation ranges from one-line convenience functions to fully custom loops, depending on your needs:

Option A: scikit-learn convenience functions (cross_val_score, cross_validate) -- handles splitting, training, and aggregation in a single call. Perfect for standard ML models and pipelines. This is the approach used by most data scientists in India and globally, and it's the right starting point for 90% of use cases.

Option B: Manual loop with scikit-learn splitters (KFold, StratifiedKFold, GroupKFold, TimeSeriesSplit) -- gives you full control over each fold's execution. Necessary when you need custom preprocessing logic, want to save per-fold models, or are working with deep learning frameworks (PyTorch, TensorFlow) that don't fit into scikit-learn's estimator API.

Option C: Deep learning CV -- manual implementation with early stopping, learning rate scheduling, and GPU management per fold. More complex but essential when evaluating neural network architectures on small-to-medium datasets.

Cost Note: Cross-validation multiplies your training cost by . For a classical ML model (XGBoost, LightGBM) that trains in 30 seconds, 5-fold CV takes 2.5 minutes -- negligible. But for a deep learning model that takes 2 hours on an A100 GPU, 5-fold CV takes 10 hours. On E2E Networks (Indian provider), that's

INR 1,700 (41). Plan accordingly: use CV for model comparison and selection, then do a single final training on the full dataset for deployment.

from sklearn.model_selection import (

cross_val_score, cross_validate, KFold, StratifiedKFold, RepeatedStratifiedKFold

)

from sklearn.ensemble import GradientBoostingClassifier

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import StandardScaler

from sklearn.impute import SimpleImputer

import numpy as np

# Build a proper pipeline (preprocessing inside CV)

pipeline = Pipeline([

('imputer', SimpleImputer(strategy='median')),

('scaler', StandardScaler()),

('model', GradientBoostingClassifier(n_estimators=200, random_state=42)),

])

# Option 1: Simple cross_val_score (stratified by default for classifiers)

scores = cross_val_score(pipeline, X, y, cv=5, scoring='f1_weighted', n_jobs=-1)

print(f"5-Fold F1: {scores.mean():.4f} (+/- {scores.std():.4f})")

# Option 2: cross_validate for multiple metrics and timing

results = cross_validate(

pipeline, X, y,

cv=StratifiedKFold(n_splits=5, shuffle=True, random_state=42),

scoring=['accuracy', 'f1_weighted', 'roc_auc'],

return_train_score=True,

n_jobs=-1,

)

for metric in ['accuracy', 'f1_weighted', 'roc_auc']:

train = results[f'train_{metric}']

test = results[f'test_{metric}']

print(f"{metric}: train={train.mean():.4f}, val={test.mean():.4f} (+/- {test.std():.4f})")

# Option 3: Repeated stratified K-fold for more stable estimates

cv = RepeatedStratifiedKFold(n_splits=5, n_repeats=3, random_state=42)

scores = cross_val_score(pipeline, X, y, cv=cv, scoring='f1_weighted', n_jobs=-1)

print(f"5x3 Repeated CV F1: {scores.mean():.4f} (+/- {scores.std():.4f})")Three progressively more robust approaches. The key pattern is wrapping preprocessing inside a Pipeline so that fitting (e.g., computing mean/std for StandardScaler) happens only on training data within each fold. Using cross_validate instead of cross_val_score gives you multiple metrics and training scores, which helps diagnose overfitting (large train-val gap). RepeatedStratifiedKFold with 3 repeats reduces variance further at the cost of 15 total model fits instead of 5.

from sklearn.model_selection import GroupKFold, StratifiedGroupKFold, cross_val_score

from sklearn.ensemble import RandomForestClassifier

import numpy as np

import pandas as pd

# Example: medical data where multiple samples come from the same patient

df = pd.read_csv('patient_data.csv')

X = df.drop(columns=['target', 'patient_id'])

y = df['target']

groups = df['patient_id'] # Ensure same patient is NEVER in both train and val

# GroupKFold: each patient appears in exactly one fold

gkf = GroupKFold(n_splits=5)

model = RandomForestClassifier(n_estimators=200, random_state=42)

scores = cross_val_score(model, X, y, cv=gkf, groups=groups, scoring='roc_auc')

print(f"GroupKFold AUC: {scores.mean():.4f} (+/- {scores.std():.4f})")

# StratifiedGroupKFold: preserve class balance AND group boundaries

sgkf = StratifiedGroupKFold(n_splits=5, shuffle=True, random_state=42)

scores = cross_val_score(model, X, y, cv=sgkf, groups=groups, scoring='roc_auc')

print(f"StratifiedGroupKFold AUC: {scores.mean():.4f} (+/- {scores.std():.4f})")

# Verify: no patient appears in both train and val for any fold

for fold_idx, (train_idx, val_idx) in enumerate(gkf.split(X, y, groups)):

train_patients = set(groups.iloc[train_idx])

val_patients = set(groups.iloc[val_idx])

overlap = train_patients & val_patients

assert len(overlap) == 0, f"Fold {fold_idx}: patient overlap detected!"

print(f"Fold {fold_idx}: {len(train_patients)} train patients, {len(val_patients)} val patients")GroupKFold is critical when your data has natural groups -- multiple blood samples from the same patient, multiple transactions from the same user (Razorpay fraud detection), or multiple images of the same product (Flipkart catalog). Without group-aware splitting, the model memorizes patient-specific or user-specific patterns and appears to generalize when it actually hasn't. The StratifiedGroupKFold variant adds class balance preservation, which is essential for medical datasets where disease prevalence is typically low.

from sklearn.model_selection import TimeSeriesSplit

import numpy as np

import pandas as pd

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.metrics import mean_absolute_error

# Load time-ordered data (e.g., Swiggy daily delivery volumes)

dates = pd.date_range('2023-01-01', periods=365, freq='D')

X = np.column_stack([

np.arange(365), # trend

np.sin(2 * np.pi * np.arange(365) / 7), # weekly seasonality

np.sin(2 * np.pi * np.arange(365) / 365), # yearly seasonality

])

y = np.random.randn(365).cumsum() + 100 # Simulated delivery volumes

# Expanding window CV (scikit-learn's TimeSeriesSplit)

tscv = TimeSeriesSplit(n_splits=5)

model = GradientBoostingRegressor(n_estimators=100, random_state=42)

for fold, (train_idx, val_idx) in enumerate(tscv.split(X)):

X_train, X_val = X[train_idx], X[val_idx]

y_train, y_val = y[train_idx], y[val_idx]

model.fit(X_train, y_train)

preds = model.predict(X_val)

mae = mean_absolute_error(y_val, preds)

print(f"Fold {fold}: Train [{train_idx[0]}-{train_idx[-1]}], "

f"Val [{val_idx[0]}-{val_idx[-1]}], MAE={mae:.2f}")

# Sliding window CV (fixed training window size)

def sliding_window_cv(n_samples, train_size, val_size, step=None):

"""Generate sliding window train/val splits for time series."""

if step is None:

step = val_size

splits = []

start = 0

while start + train_size + val_size <= n_samples:

train_idx = np.arange(start, start + train_size)

val_idx = np.arange(start + train_size, start + train_size + val_size)

splits.append((train_idx, val_idx))

start += step

return splits

# Use fixed 180-day training window, 30-day validation window

splits = sliding_window_cv(len(X), train_size=180, val_size=30, step=30)

for fold, (train_idx, val_idx) in enumerate(splits):

model.fit(X[train_idx], y[train_idx])

preds = model.predict(X[val_idx])

mae = mean_absolute_error(y[val_idx], preds)

print(f"Sliding Fold {fold}: Train [{train_idx[0]}-{train_idx[-1]}], "

f"Val [{val_idx[0]}-{val_idx[-1]}], MAE={mae:.2f}")Time-series CV respects temporal ordering -- the model is never trained on future data and evaluated on past data, which would be data leakage. scikit-learn's TimeSeriesSplit implements the expanding window approach (training window grows with each fold). The custom sliding_window_cv function implements a fixed-size sliding window, which is better when you believe recent data is more relevant than distant history -- common in production scenarios like Swiggy's delivery time prediction or Zerodha's market pattern detection.

from sklearn.model_selection import StratifiedKFold, GridSearchCV, cross_val_score

from sklearn.ensemble import RandomForestClassifier, GradientBoostingClassifier

from sklearn.svm import SVC

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import StandardScaler

import numpy as np

# Inner CV: hyperparameter tuning

# Outer CV: unbiased performance estimation

def nested_cv_compare(X, y, models_and_params, outer_cv=5, inner_cv=3):

"""Compare multiple models using nested cross-validation."""

outer = StratifiedKFold(n_splits=outer_cv, shuffle=True, random_state=42)

results = {}

for name, (pipeline, param_grid) in models_and_params.items():

# Inner CV is wrapped inside GridSearchCV

inner = StratifiedKFold(n_splits=inner_cv, shuffle=True, random_state=42)

search = GridSearchCV(

pipeline, param_grid,

cv=inner, scoring='f1_weighted', n_jobs=-1, refit=True

)

# Outer CV evaluates the entire search procedure

outer_scores = cross_val_score(

search, X, y, cv=outer, scoring='f1_weighted', n_jobs=1

)

results[name] = outer_scores

print(f"{name}: {outer_scores.mean():.4f} (+/- {outer_scores.std():.4f})")

return results

# Define models with their search spaces

models_and_params = {

'RandomForest': (

Pipeline([('scaler', StandardScaler()), ('model', RandomForestClassifier(random_state=42))]),

{'model__n_estimators': [100, 300], 'model__max_depth': [5, 10, None]}

),

'GBM': (

Pipeline([('scaler', StandardScaler()), ('model', GradientBoostingClassifier(random_state=42))]),

{'model__n_estimators': [100, 300], 'model__learning_rate': [0.01, 0.1]}

),

'SVM': (

Pipeline([('scaler', StandardScaler()), ('model', SVC(random_state=42))]),

{'model__C': [0.1, 1, 10], 'model__kernel': ['rbf', 'linear']}

),

}

results = nested_cv_compare(X, y, models_and_params)

# Statistical comparison

best_name = max(results, key=lambda k: results[k].mean())

print(f"\nBest model: {best_name}")

for name, scores in results.items():

print(f" {name}: {scores.mean():.4f} +/- {scores.std():.4f} [{', '.join(f'{s:.4f}' for s in scores)}]")Nested cross-validation is the gold standard when you need to both tune hyperparameters and report an unbiased performance estimate. The inner loop (GridSearchCV) handles model selection within each outer fold's training data, while the outer loop evaluates the entire tuning procedure on held-out data. Without nesting, the CV score from GridSearchCV is optimistically biased -- Varma & Simon (2006) showed this bias can be 2-5% for small datasets. The cost is model fits, so keep the grid small or use RandomizedSearchCV for the inner loop.

from sklearn.model_selection import cross_val_score, StratifiedKFold

from sklearn.preprocessing import StandardScaler

from sklearn.linear_model import LogisticRegression

from sklearn.pipeline import Pipeline

import numpy as np

np.random.seed(42)

X = np.random.randn(500, 20)

y = (X[:, 0] + X[:, 1] > 0).astype(int)

cv = StratifiedKFold(n_splits=5, shuffle=True, random_state=42)

# WRONG: Scale BEFORE cross-validation (data leakage!)

scaler = StandardScaler()

X_scaled_leaked = scaler.fit_transform(X) # Sees ALL data including future val folds

scores_leaked = cross_val_score(

LogisticRegression(), X_scaled_leaked, y, cv=cv, scoring='accuracy'

)

print(f"LEAKED: {scores_leaked.mean():.4f} (+/- {scores_leaked.std():.4f})")

# RIGHT: Scale INSIDE cross-validation (via Pipeline)

pipeline = Pipeline([

('scaler', StandardScaler()),

('model', LogisticRegression()),

])

scores_correct = cross_val_score(pipeline, X, y, cv=cv, scoring='accuracy')

print(f"CORRECT: {scores_correct.mean():.4f} (+/- {scores_correct.std():.4f})")

# The difference might be small here, but with feature selection or

# target encoding, the leakage effect can be dramatic (5-15% inflation)

print(f"\nLeakage inflation: {(scores_leaked.mean() - scores_correct.mean()) * 100:.2f}%")This example demonstrates the most common cross-validation mistake: preprocessing outside the CV loop. When you fit a StandardScaler on the entire dataset before splitting, the validation fold's statistics leak into the training process. For simple scaling, the effect is small (0.1-0.5%). But for feature selection (selecting features based on correlation with the target) or target encoding (encoding categories using the mean target value), the leakage can inflate scores by 5-15%, leading to catastrophically wrong model selection decisions. Always use sklearn.pipeline.Pipeline to keep preprocessing inside the fold.

# Cross-validation configuration (YAML equivalent)

cross_validation:

strategy: stratified_kfold # kfold | stratified_kfold | group_kfold | time_series | repeated_stratified

n_splits: 5

n_repeats: 1 # >1 for repeated CV

shuffle: true

random_state: 42

scoring:

primary: f1_weighted

additional:

- accuracy

- roc_auc

- precision_weighted

- recall_weighted

pipeline:

preprocessing:

- type: SimpleImputer

strategy: median

- type: StandardScaler

model:

type: GradientBoostingClassifier

params:

n_estimators: 200

max_depth: 5

learning_rate: 0.1

nested_cv: # Optional: for hyperparameter tuning

enabled: false

inner_cv:

strategy: stratified_kfold

n_splits: 3

search:

type: RandomizedSearchCV

n_iter: 50

scoring: f1_weighted

group_column: null # Set to column name for GroupKFold

time_column: null # Set to column name for TimeSeriesSplit

output:

save_oof_predictions: true # Out-of-fold predictions for stacking

save_fold_models: false # Save each fold's trained model

report_train_scores: true # Track overfitting via train-val gapCommon Implementation Mistakes

- ●

Preprocessing outside the fold: Fitting scalers, encoders, or feature selectors on the full dataset before running CV leaks validation information into training. This is the #1 cause of inflated CV scores. Always wrap preprocessing in a

Pipelineor perform it manually inside the fold loop. - ●

Ignoring group structure: When data has natural groups (same patient, same user, same product), standard KFold allows the same group to appear in both train and validation, leading to overly optimistic estimates. Use

GroupKFoldorStratifiedGroupKFoldwhenever groups exist. - ●

Using random K-fold for time series: Randomly splitting temporal data lets the model train on future data and predict the past, which is nonsensical for forecasting. Use

TimeSeriesSplitor a custom sliding window splitter for any data with temporal ordering. - ●

Reporting CV score as deployment performance: The CV score estimates the performance of your procedure, not your final model. The final model is trained on all data and may be slightly better (less bias). Report the held-out test set score as your deployment performance estimate.

- ●

Too few folds for small datasets: With 100 samples and 5-fold CV, each validation fold has only 20 samples. The per-fold scores will have high variance. Use 10-fold or repeated K-fold for small datasets to get more stable estimates.

- ●

Confusing CV with test set evaluation: CV is for model development decisions (which model? which features? which hyperparameters?). The test set is for final reporting. Using the test set during development defeats its purpose.

When Should You Use This?

Use When

Your dataset has fewer than 50,000 samples, where the variance of a single holdout split is high enough to produce misleading performance estimates

You need to compare two or more models (or configurations) and the expected performance difference is small (1-3%), requiring low-variance estimates to make a reliable decision

You are performing hyperparameter tuning -- CV is the standard evaluation signal for the inner loop of any HPO method (GridSearchCV, RandomizedSearchCV, Bayesian optimization)

Regulatory or compliance requirements demand statistically rigorous model evaluation -- common in healthcare (ICMR guidelines), finance (RBI model risk management), and insurance

You want to generate out-of-fold predictions for model stacking (blending) or for building reliable calibration curves

You are working with imbalanced data where a single random split might misrepresent the minority class in the validation set

Avoid When

Your dataset is very large (millions of samples) and a single well-stratified holdout set already provides a low-variance performance estimate -- the marginal benefit of K-fold CV does not justify the K-fold increase in training cost

Training is extremely expensive (e.g., full fine-tuning a 70B parameter LLM takes 3 days on 8 A100s) and you cannot afford to multiply that cost by K -- use a single large holdout set instead

You are doing rapid prototyping / exploratory analysis where an approximate performance signal is sufficient to decide whether to invest further in a particular direction

Your data has extreme temporal dynamics and a single train/test split at a well-chosen time boundary gives a more realistic evaluation than averaged time-series CV folds

You are evaluating a pre-trained model (like GPT-4 or a downloaded Hugging Face checkpoint) where no training occurs and evaluation is just inference -- a single evaluation pass is sufficient

The data generation process is highly non-stationary and older folds would train on data from a fundamentally different distribution than the current one -- time-series CV or a single recent holdout is better

Key Tradeoffs

Bias vs. Variance: The K Knob

The choice of is the primary tradeoff in cross-validation:

| K Value | Training Set Size | Bias | Variance | Compute Cost | Best For |

|---|---|---|---|---|---|

| K=2 | 50% of data | High (pessimistic) | Low | 2x | Very large datasets |

| K=5 | 80% of data | Low-Medium | Low-Medium | 5x | Default for most problems |

| K=10 | 90% of data | Low | Medium | 10x | Small-medium datasets |

| K=n (LOO) | n-1 samples | Minimal | High | nx | Tiny datasets, linear models |

| 5x3 Repeated | 80% of data | Low | Very Low | 15x | When stability matters |

The standard recommendation is K=5 for large datasets (>10K samples) and K=10 for smaller ones (<10K). For very small datasets (under 200 samples), repeated K-fold (e.g., 10-fold repeated 5 times) or leave-one-out may be necessary.

Stratified vs. Standard: Almost Always Stratify

For classification tasks, always use stratified K-fold unless you have a specific reason not to. The cost of stratification is zero (it's just a smarter split), and the benefit is significant for imbalanced datasets. With 5% positive rate and 5-fold CV, a random split might give folds with 3% to 7% positive rate, creating inconsistent evaluation conditions.

CV Score vs. Test Set Score

The CV score and the test set score answer different questions. The CV score estimates how well your modeling procedure generalizes. The test set score estimates how well your final model generalizes. The test set score is typically slightly higher than the CV score because the final model is trained on more data (all of the training set rather than K-1/K of it).

Rule of Thumb: If your CV score and test score differ by more than 2-3 standard deviations of the CV estimate, something may be wrong -- data leakage, distribution shift, or overfitting the validation folds during model selection.

Alternatives & Comparisons

A single holdout split is faster (1 model fit vs. K) and simpler to implement. It is sufficient for very large datasets where the holdout set is big enough to provide a low-variance estimate. Use a single split for rapid prototyping or when training is prohibitively expensive; switch to CV when you need statistically reliable model comparisons or when working with small to medium datasets.

Cross-validation and hyperparameter tuning are complementary, not alternatives. CV provides the evaluation signal that HPO optimizes against. Most HPO methods (GridSearchCV, RandomizedSearchCV, Optuna) use CV internally to score each hyperparameter configuration. The choice is not CV vs. HPO; it is whether to use CV or a single holdout as the evaluation method within HPO.

Bootstrap evaluation draws random samples with replacement from the training data, training on each bootstrap sample and evaluating on the out-of-bag samples. It provides similar information to CV but has slightly more pessimistic bias (each bootstrap sample contains only ~63.2% of unique training points). Use bootstrap when you want confidence intervals on your metric or when the dataset is very small (<100 samples). Use CV for most other situations.

Pros, Cons & Tradeoffs

Advantages

Robust performance estimation -- averaging across K folds dramatically reduces the variance of the performance estimate compared to a single holdout split, giving you much higher confidence in your model comparison decisions

Efficient use of limited data -- every sample serves as both training and validation data (across different folds), which is critical when data is expensive to collect (medical imaging, rare-event fraud detection at Razorpay, low-resource Indian language NLP)

Out-of-fold predictions -- CV produces a prediction for every training sample (from a model that didn't see it), enabling model stacking, reliable calibration curves, and threshold optimization without needing additional data

Standard and well-understood -- CV is the universally accepted evaluation methodology in both industry and academia. Reviewers, regulators, and stakeholders understand and trust CV results, which simplifies communication

Flexible family of techniques -- stratified, grouped, temporal, nested, and repeated variants handle nearly every data structure you'll encounter in practice, from i.i.d. tabular data to grouped medical records to time-ordered financial transactions

Detects overfitting -- by comparing train-fold and val-fold scores, CV reveals the generalization gap. A large gap (e.g., 99% train accuracy vs. 85% val accuracy) is a clear signal of overfitting that a single holdout might miss if it's an unusually easy split

Enables statistical testing -- with K performance scores, you can compute confidence intervals and perform paired statistical tests (corrected paired t-test, Wilcoxon signed-rank) to determine if one model is significantly better than another

Disadvantages

Computational cost scales linearly with K -- 5-fold CV requires 5 full training runs. For expensive models (deep learning, large ensembles), this can be prohibitive. A 2-hour training run becomes 10 hours with 5-fold CV, costing ~INR 1,700 on an A100 at E2E Networks rates

Does not produce a single deployable model -- CV produces K models and an aggregate score, but you still need to train one final model on the full dataset for deployment. The CV score is an estimate of the final model's performance, not its actual performance

Variance between folds can be high for small datasets -- with 200 samples and 5-fold CV, each validation fold has only 40 samples. Individual fold scores may swing widely, and the mean can still be noisy. Repeated CV mitigates this but multiplies cost further

Easy to introduce data leakage -- any preprocessing done before CV (fitting scalers, selecting features, encoding targets) leaks information and inflates scores. This is the most common source of inflated metrics in Kaggle competitions and industry alike

Not suitable for all data types without modification -- naive application to time series, grouped data, or streaming data produces misleading results. You must use the appropriate splitter variant (TimeSeriesSplit, GroupKFold), which requires domain knowledge

Can overfit the validation folds during extensive model selection -- if you run 100 different model configurations with 5-fold CV, the best configuration may have exploited noise in the CV estimate. Nested CV or a held-out test set guards against this

Failure Modes & Debugging

Data leakage through preprocessing outside folds

Cause

Fitting preprocessing steps (StandardScaler, PCA, feature selection, target encoding) on the full dataset before splitting into folds. The validation fold's distribution information leaks into the training fold through the shared fitted transformer.

Symptoms

CV scores are consistently higher than held-out test set performance. The gap widens with more aggressive preprocessing (e.g., mutual information feature selection or target encoding can inflate scores by 5-15%). Performance in production is significantly worse than CV suggested.

Mitigation

Always wrap preprocessing inside a sklearn.pipeline.Pipeline. This ensures that .fit() is called only on training fold data, and .transform() is applied to both training and validation folds independently. Audit your pipeline: any fit_transform() call that touches the full dataset before CV is a potential leak.

Ignoring group structure (duplicate leakage)

Cause

When data contains natural groups (same patient, same user, same product), standard KFold can assign different samples from the same group to both training and validation folds. The model memorizes group-specific patterns that look like generalization.

Symptoms

CV score is unrealistically high compared to performance on genuinely new groups. For example, a medical model might achieve 95% AUC in CV but only 78% AUC when evaluated on patients from a new hospital. User-level fraud detection at Razorpay shows similar patterns when user-level splits are not enforced.

Mitigation

Identify all group structures in your data: patient IDs, user IDs, session IDs, geographic clusters, temporal groups. Use GroupKFold or StratifiedGroupKFold to ensure group-level isolation. If in doubt about whether groups matter, run both standard and group-aware CV and compare -- a large gap indicates leakage.

Temporal leakage in time-series data

Cause

Using random K-fold on time-ordered data allows the model to train on future data and predict past data ("look-ahead bias"). This is particularly insidious because the leaked information is the future state of the system, which is exactly what you want to predict.

Symptoms

CV scores for time-series prediction tasks are much higher than production performance. Models show degraded performance after deployment, especially during regime changes (market shifts, seasonal transitions). Swiggy's delivery time models, for instance, must respect temporal ordering or risk learning patterns from festival-period data that don't apply to regular days.

Mitigation

Use TimeSeriesSplit (expanding window) or a custom sliding window splitter. Ensure that all features used are available at prediction time -- lag features computed from the validation period are another subtle form of temporal leakage. Add an explicit embargo period (gap) between train and validation to handle features with delayed availability.

Overfitting the CV procedure during extensive model selection

Cause

Running many model configurations (50-200+) with the same K-fold CV splits effectively searches for configurations that happen to score well on these specific folds, overfitting the CV estimate itself.

Symptoms

The best CV score from a large search is optimistically biased -- it overestimates the true generalization performance. This is analogous to multiple hypothesis testing without correction. The gap between the selected model's CV score and its test set performance widens as more configurations are tried.

Mitigation

Use nested cross-validation: the inner loop handles model selection (hyperparameter tuning), while the outer loop provides an unbiased performance estimate. Alternatively, hold out a final test set that is never used during any model selection step. Limit the total number of configurations tested to a reasonable budget.

Class imbalance causing fold degeneration

Cause

For highly imbalanced datasets (e.g., 0.5% fraud rate at Razorpay), random K-fold may produce folds where the minority class has 0 or 1 samples, making validation metrics undefined or meaningless.

Symptoms

Per-fold metrics show extreme variability (one fold has F1=0.0, another has F1=0.8). Some folds raise warnings about undefined metrics. The mean CV score is unreliable due to averaging over degenerate folds.

Mitigation

Use StratifiedKFold to ensure each fold maintains the class distribution. For extreme imbalance (<1%), consider stratified repeated K-fold for additional stability, or use metrics that are well-defined even with few positive samples (ROC-AUC rather than precision at a specific threshold). If the minority class has fewer than K*2 samples, LOOCV or stratified bootstrap may be more appropriate than K-fold.

Inconsistent fold sizes causing biased aggregation

Cause

When the number of samples is not perfectly divisible by K, or when stratification constraints produce unequal folds, naively averaging per-fold scores gives disproportionate weight to larger or smaller folds.

Symptoms

The CV mean score differs slightly from what you'd get by computing the metric on the concatenated out-of-fold predictions. This discrepancy is usually small (<0.5%) but can matter for reporting and regulatory purposes.

Mitigation

Compute metrics on the concatenated out-of-fold predictions rather than averaging per-fold scores when fold sizes are unequal. In scikit-learn, use cross_val_predict to get all OOF predictions, then compute a single metric on the full set. Alternatively, use weighted averaging where each fold's score is weighted by its sample count.

Placement in an ML System

Where Does It Sit in the Pipeline?

Cross-validation sits at the intersection of data splitting and model training in the ML pipeline. It operates on the training partition (after the initial train/test split) and serves as the primary feedback mechanism for all model development decisions.

The typical workflow is: raw data -> preprocessing -> train/test split -> cross-validation on training set (for model comparison, hyperparameter tuning, feature selection) -> final training on full training set -> test set evaluation -> deploy.

Cross-validation is tightly coupled with hyperparameter tuning: every call to GridSearchCV or RandomizedSearchCV runs CV internally. It is also the foundation of model stacking: the out-of-fold predictions from K-fold CV become the training data for the meta-learner.

In production ML systems at companies like Flipkart and Swiggy, cross-validation is typically a step in an automated pipeline (Kubeflow, Airflow, or custom orchestrators) that runs whenever new training data arrives. The CV scores are logged alongside the model version in the model registry, providing an audit trail of how each model was evaluated before deployment.

Key Insight: Cross-validation is fundamentally an evaluation technique, but its outputs (fold scores, OOF predictions, fold models) feed into many downstream processes. Think of it as the quality gate that every model must pass through before being considered for production.

Pipeline Stage

Training / Model Evaluation

Upstream

- train-test-split

- feature-engineering

- data-validation

Downstream

- hyperparameter-tuning

- model-training

- model-registry

Scaling Bottlenecks

The primary bottleneck is training cost multiplied by K. Cross-validation is embarrassingly parallel (all K folds are independent), so the wall-clock cost can be reduced to the cost of a single fold if you have K workers. But the total compute cost is fixed at K times the training cost.

For classical ML (XGBoost, LightGBM, RandomForest, SVM): training takes seconds to minutes, and 5-10 fold CV is nearly free. A 200-feature, 100K-row tabular dataset takes ~30 seconds per fold for XGBoost. 5-fold CV: 2.5 minutes total. This is the sweet spot for CV.

For deep learning on medium datasets: a ResNet50 on 50K images takes ~30 minutes per fold on a V100 GPU. 5-fold CV: 2.5 hours. On E2E Networks (V100 at INR 90/hr), that's INR 225 ($2.70). Affordable, and often worth the improved model selection.

For large-scale deep learning: fine-tuning a 7B LLM with LoRA takes 2-4 hours per fold on an A100. 5-fold CV: 10-20 hours = INR 1,700-3,400 (~40-80) on AWS Mumbai. This is where you start questioning whether CV is worth it -- often, a well-chosen single holdout with multiple random seeds is more cost-effective.

The second bottleneck is memory: each fold trains a separate model, and if you're saving per-fold models for ensembling or analysis, the storage adds up. With 5 XGBoost models at 500MB each, that's 2.5GB. With 5 fine-tuned LLM adapters at 200MB each, that's 1GB -- manageable but worth planning for.

Production Case Studies

Flipkart's product recommendation and search ranking systems serve hundreds of millions of users across diverse product categories. Their ML team uses stratified cross-validation to evaluate ranking models across product categories, ensuring that evaluation is representative of the highly heterogeneous catalog. With multiple models serving different category verticals, cross-validation provides comparable performance metrics that enable apples-to-apples model comparisons.

Cross-validation enabled Flipkart's team to reliably measure 1-2% improvements in click-through rate across recommendation model iterations, improvements that would have been lost in the noise of a single holdout split. The standardized CV-based evaluation framework reduced the model development cycle from weeks of A/B testing to days of offline validation.

Swiggy's delivery time prediction system uses a MIMO deep learning model that predicts multiple time components (order-to-assignment, first mile, wait time, last mile). They employ time-series cross-validation with expanding windows to evaluate model performance across different time periods, respecting temporal ordering and seasonal patterns (festival seasons like Diwali and Big Billion Days cause distribution shifts).

Time-series CV prevented Swiggy from deploying models that performed well on average historical data but failed during high-demand periods. The expanding window approach also revealed that model performance degrades over time without retraining, providing quantitative justification for their weekly retraining schedule.

Razorpay's fraud detection system processes millions of transactions and must distinguish legitimate purchases from fraudulent ones. They use StratifiedGroupKFold cross-validation -- stratified to handle the extreme class imbalance (fraud rate <1%) and grouped by merchant/user to prevent data leakage from the same entity appearing in both train and validation. Their real-time ML system (built on Apache Flink) uses CV-validated models for millisecond-level fraud scoring.

Group-aware stratified CV revealed that standard KFold was overestimating fraud detection precision by 8-12% due to merchant-level leakage. After switching to StratifiedGroupKFold, the offline CV scores aligned much more closely with production metrics, enabling more reliable model deployment decisions and reducing false positive rates that affected legitimate merchants.

Netflix's recommendation team uses sophisticated offline evaluation methods to assess ranking models before committing to expensive A/B tests. Their offline evaluation combines time-aware cross-validation (to avoid temporal leakage in viewing patterns) with user-level grouping (to prevent the same user's views from appearing in both train and evaluation). The team has published extensively on the challenges of offline evaluation for recommender systems, including the gap between offline CV metrics and online engagement metrics.

Netflix's rigorous offline evaluation methodology reduced the number of A/B tests needed by filtering out model changes that showed no significant improvement in time-aware CV. Given that each A/B test requires weeks of runtime across millions of users, reducing unnecessary tests saves substantial engineering resources and prevents exposing users to inferior recommendation models.

Tooling & Ecosystem

The standard cross-validation library for Python ML. Provides cross_val_score, cross_validate, cross_val_predict, and a comprehensive family of splitters: KFold, StratifiedKFold, GroupKFold, StratifiedGroupKFold, TimeSeriesSplit, RepeatedKFold, RepeatedStratifiedKFold, LeaveOneOut, LeavePOut, ShuffleSplit, and more. Integrates seamlessly with Pipeline for leak-free evaluation.

Hyperparameter optimization framework that uses cross-validation as its evaluation signal. Optuna's OptunaSearchCV class provides a drop-in replacement for scikit-learn's GridSearchCV with Bayesian optimization. The integration of CV evaluation with intelligent search makes it the recommended tool for combined CV + HPO workflows.

XGBoost's xgb.cv() function provides native cross-validation with early stopping based on the CV metric, which is more efficient than running scikit-learn's CV wrapper because it performs early stopping within the CV loop. Supports stratified splitting and custom evaluation metrics.

Similar to XGBoost, LightGBM's lgb.cv() provides native cross-validation with early stopping. The native implementation is significantly faster than wrapping LightGBM in scikit-learn's CV because it avoids redundant data loading and supports GPU acceleration across folds.

Experiment tracking platform that integrates with cross-validation workflows. Neptune logs per-fold metrics, hyperparameters, and artifacts, providing dashboards to compare CV results across experiments. Useful for teams that need to track hundreds of CV experiments over time.

Visual diagnostic library for scikit-learn that provides CVScores visualizer -- a visual wrapper around cross-validation that plots per-fold scores as a bar chart with mean/std overlay. Helps diagnose fold-to-fold variability and identify problematic folds at a glance.

Research & References

Arlot & Celisse (2010)Statistics Surveys, Vol. 4

The definitive survey of cross-validation theory and practice. Covers leave-one-out, leave-p-out, V-fold, repeated, and Monte Carlo CV. Provides theoretical analysis of bias-variance tradeoffs for different K values and guidelines for choosing the best CV procedure based on problem characteristics.

Raschka (2018)arXiv preprint

Comprehensive practical guide to model evaluation including holdout, bootstrap, K-fold CV, nested CV, and statistical comparison tests. Discusses the bias-variance tradeoff in CV and provides recommendations for choosing K. The go-to reference for practitioners who want to understand why different evaluation approaches exist.

Varma & Simon (2006)BMC Bioinformatics, Vol. 7

Demonstrated that using CV for both model selection and performance estimation produces optimistically biased error estimates. Proposed nested cross-validation as the solution, showing it produces nearly unbiased estimates. Essential reading for anyone doing hyperparameter tuning with CV.

Bergmeir, Hyndman & Koo (2018)Computational Statistics & Data Analysis, Vol. 120

Provided theoretical justification for using standard K-fold CV (not just time-series split) for autoregressive models when the errors are uncorrelated. Challenged the conventional wisdom that standard CV is always invalid for time series, showing that for many ML models with uncorrelated residuals, it performs well.

Dietterich (1998)Neural Computation, Vol. 10

Analyzed the statistical properties of tests based on cross-validation for comparing classifiers. Showed that paired t-tests on 10-fold CV have elevated Type I error rates and recommended the 5x2 cross-validation paired t-test as a more reliable alternative. Foundational work on statistical rigor in model comparison.

Stone (1974)Journal of the Royal Statistical Society: Series B, Vol. 36

The foundational paper that formalized cross-validation as a model selection criterion. Showed that leave-one-out CV is asymptotically equivalent to AIC (Akaike's Information Criterion) for linear models, establishing the theoretical connection between CV and information-theoretic model selection.

Interview & Evaluation Perspective

Common Interview Questions

- ●

What is K-fold cross-validation and why is it preferred over a single holdout split?

- ●

How do you choose the value of K? What are the tradeoffs between K=5, K=10, and leave-one-out?

- ●

Explain data leakage in the context of cross-validation. How does preprocessing outside the fold cause leakage?

- ●

When would you use StratifiedKFold vs. GroupKFold vs. TimeSeriesSplit?

- ●

What is nested cross-validation and when is it necessary?

- ●

You have a dataset of 500 patients with 10 blood samples each. How would you set up cross-validation?

- ●

Is cross-validation necessary for a dataset with 10 million samples? Why or why not?

- ●

How would you use cross-validation for time-series forecasting at Swiggy or Uber?

Key Points to Mention

- ●

The bias-variance tradeoff in choosing K: small K has pessimistic bias (less training data per fold), large K has high variance (correlated folds). K=5 and K=10 are standard because they balance this tradeoff empirically.

- ●

Data leakage through preprocessing outside folds is the #1 practical pitfall. Always use

sklearn.pipeline.Pipelineto ensurefit()runs only on training fold data -- name this pattern explicitly and explain why it matters. - ●

Stratified K-fold should be the default for classification -- it costs nothing extra and prevents degenerate folds for imbalanced datasets. GroupKFold is essential when data has natural groups (patients, users, sessions).

- ●

Nested CV is required when you use CV for both model selection and performance estimation. The inner loop tunes hyperparameters; the outer loop estimates generalization. Without nesting, the CV score is optimistically biased (Varma & Simon, 2006).

- ●

Know when CV is overkill: very large datasets (millions of samples), extremely expensive training (LLM fine-tuning), or rapid prototyping. A single well-stratified holdout with multiple random seeds is often sufficient in these cases.

- ●

Out-of-fold predictions are a powerful output of CV -- they enable model stacking, reliable calibration, and threshold optimization without additional data.

Pitfalls to Avoid

- ●

Saying LOOCV is always the best choice because it uses the most training data -- interviewers expect you to mention its high variance and computational cost, and to know that K=5 or K=10 is usually better in practice

- ●

Not mentioning data leakage -- this is a red flag in any CV discussion. Even if the interviewer doesn't ask, proactively mention the Pipeline pattern to show depth

- ●

Applying random K-fold to time-series data without discussing temporal ordering -- this immediately signals lack of production experience

- ●

Confusing cross-validation with bootstrapping -- they are different resampling techniques with different properties. CV partitions the data; bootstrap samples with replacement

- ●

Claiming cross-validation produces a deployable model -- it produces an estimate of performance, not a model. The final model is trained on all training data after CV-guided selection

Senior-Level Expectation

A senior candidate should demonstrate mastery beyond basic K-fold. They should discuss GroupKFold for data with natural groups (and give a concrete example from their domain), nested CV for unbiased evaluation during hyperparameter search, and TimeSeriesSplit for temporal data. They should articulate the data leakage taxonomy: preprocessing leakage, group leakage, and temporal leakage, with specific examples of each. Cost analysis is expected: when is 5-fold CV worth the 5x compute cost vs. a single holdout? At what dataset size does the benefit diminish? Senior engineers should also discuss out-of-fold predictions for model stacking, calibration, and threshold selection. They should know the statistical limitations: Dietterich (1998) showed that paired t-tests on CV scores have elevated Type I error, so simple t-tests on fold scores are not statistically sound for model comparison. Finally, they should be able to discuss when CV is the wrong tool: non-stationary distributions, extremely large datasets, or compute-constrained settings where a single holdout with confidence intervals is more practical.

Summary

Cross-validation is the cornerstone of honest model evaluation in machine learning. At its core, it systematically partitions your data into multiple train/validation splits, trains and evaluates on each split, and averages the results to produce a low-variance estimate of how well your model will generalize. The technique comes in many variants -- K-fold for general use, StratifiedKFold for classification with imbalanced classes, GroupKFold for data with natural groups (patients, users, merchants), TimeSeriesSplit for temporal data, and nested CV for combining model selection with unbiased performance estimation.

The most critical practical lesson is data leakage prevention: any preprocessing, feature computation, or data transformation that touches validation fold data before the fold's training step will inflate your performance estimates, sometimes dramatically. The solution is simple -- use sklearn.pipeline.Pipeline to encapsulate all preprocessing within each fold -- but the failure to do so remains the single most common source of inflated metrics in both industry and academic ML. Group leakage and temporal leakage are equally important variants that require GroupKFold and TimeSeriesSplit respectively.

For Indian ML teams, the key tradeoff is compute cost vs. evaluation quality. For classical ML on tabular data (the bread and butter of companies like Razorpay, Zerodha, and Flipkart's analytics teams), 5-10 fold CV is essentially free and should always be used. For deep learning on medium datasets, 5-fold CV at ~INR 1,700 per run on E2E Networks is a reasonable investment for model selection decisions. For large-scale deep learning and LLM fine-tuning, a well-chosen single holdout with multiple random seeds is often the pragmatic choice, with CV reserved for final publication-quality evaluation.

Cross-validation is not just a technique -- it is a discipline of intellectual honesty in model evaluation. The moment you rely on a single number from a single split, you are gambling that one random partition of your data is representative. CV turns that gamble into a systematic estimation procedure with quantified uncertainty.